Private student loans (PSLs) are typically far more risky and expensive for consumers seeking a way to pay for college than federally-backed student loans. Private student loans, like credit cards, generally offer variable interest rates that are higher for those borrowers with the least means. The Consumer Financial Protection Bureau's (CFPB) Consumer Complaint Database sheds light on the problems borrowers face with private student loans and enables the public to evaluate which lenders and servicers receive the most complaints. Private Loans, Public Complaints is the second in a series of reports examining patterns in complaints to the CFPB about various sectors of the financial services industry and how those complaints are resolved.

The Consumer Financial Protection Bureau (CFPB) was established in 2010 in the wake of the worst financial crisis in decades. Its mission is to identify dangerous and unfair financial practices, to educate consumers about these practices, and to regulate the financial institutions that perpetuate them.

To help accomplish these goals, the CFPB has created and made available to the public the Consumer Complaint Database. The database tracks complaints made by consumers to the CFPB and how they are resolved. The Consumer Complaint Database enables the CFPB to identify financial practices that threaten to harm consumers and enables the public to evaluate both the performance of the financial industry and of the CFPB.

This report is the second of several that will review complaints to the CFPB nationally and on a state-by-state level. In this report we explore consumer complaints in the private student loan sector with the aim of uncovering patterns in the problems consumers are experiencing with their student loans.

Student consumers can obtain federal student loans, private student loans or both to pay for higher education. Private student loans (PSLs) are typically far more risky and expensive for consumers seeking a way to pay for college. Private student loans, like credit cards, generally offer variable interest rates that are higher for those borrowers with the least means. Repayment options are also severely limited. Federal student loans, by contrast, are typically subsidized at a fixed interest rate and offer repayment options like deferment, income-based repayment and loan forgiveness that can help the borrowers respond to job changes, job loss, illness or other changes in income.

PSLs accounted for about 7 percent of all student education loans taken out last year, and account for 15 percent of outstanding student loan debt in the United States. The current debt owed by consumers in the United States on their private student loans is estimated to be approximately $165 billion.

Since the Consumer Financial Protection Bureau began collecting data on private student loans in March 2012, the CFPB has recorded more than 4,300 complaints about problems with private student loans.*

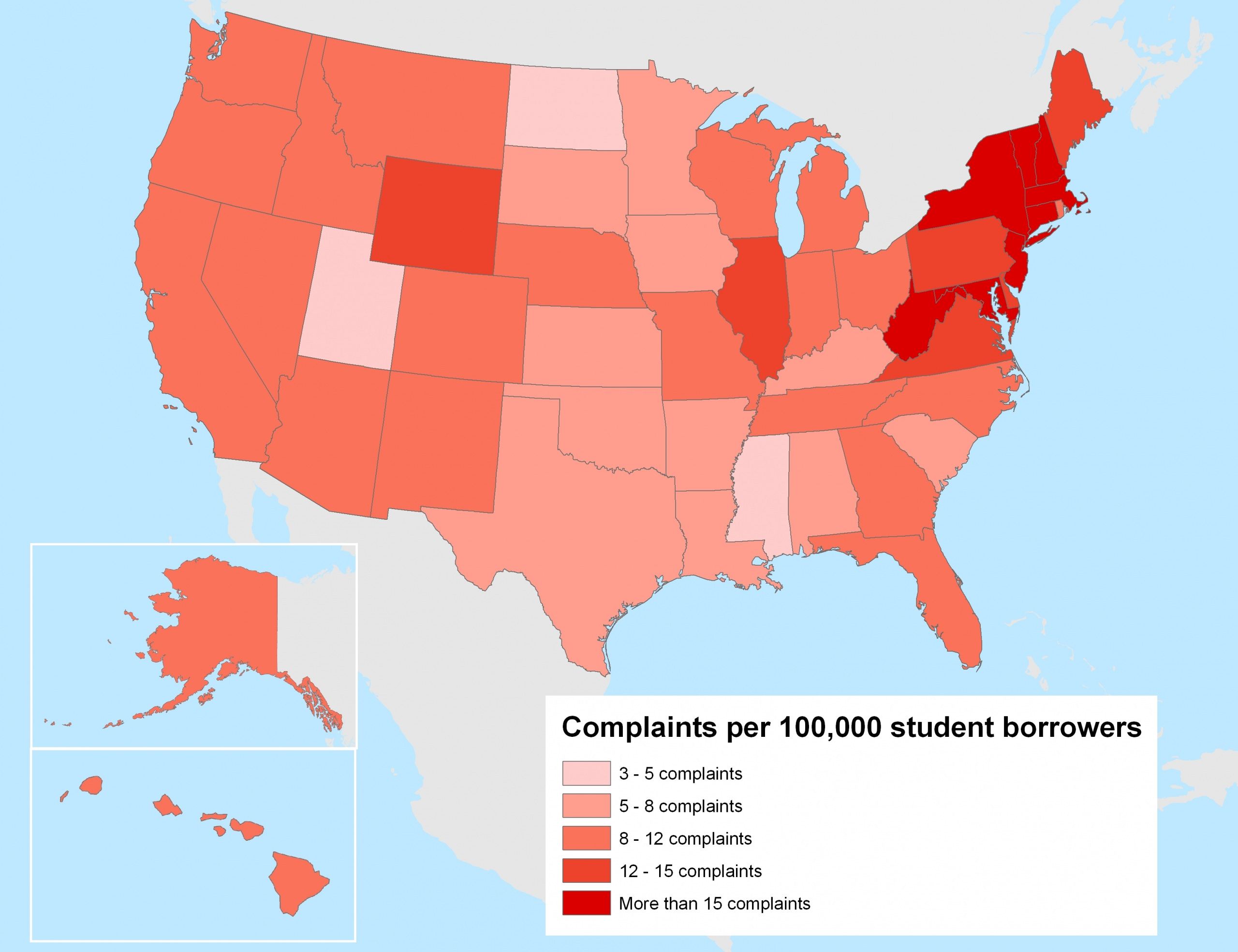

Complaints about private student loans vary by state, and state residents vary in their tendency to reach out to the CFPB.

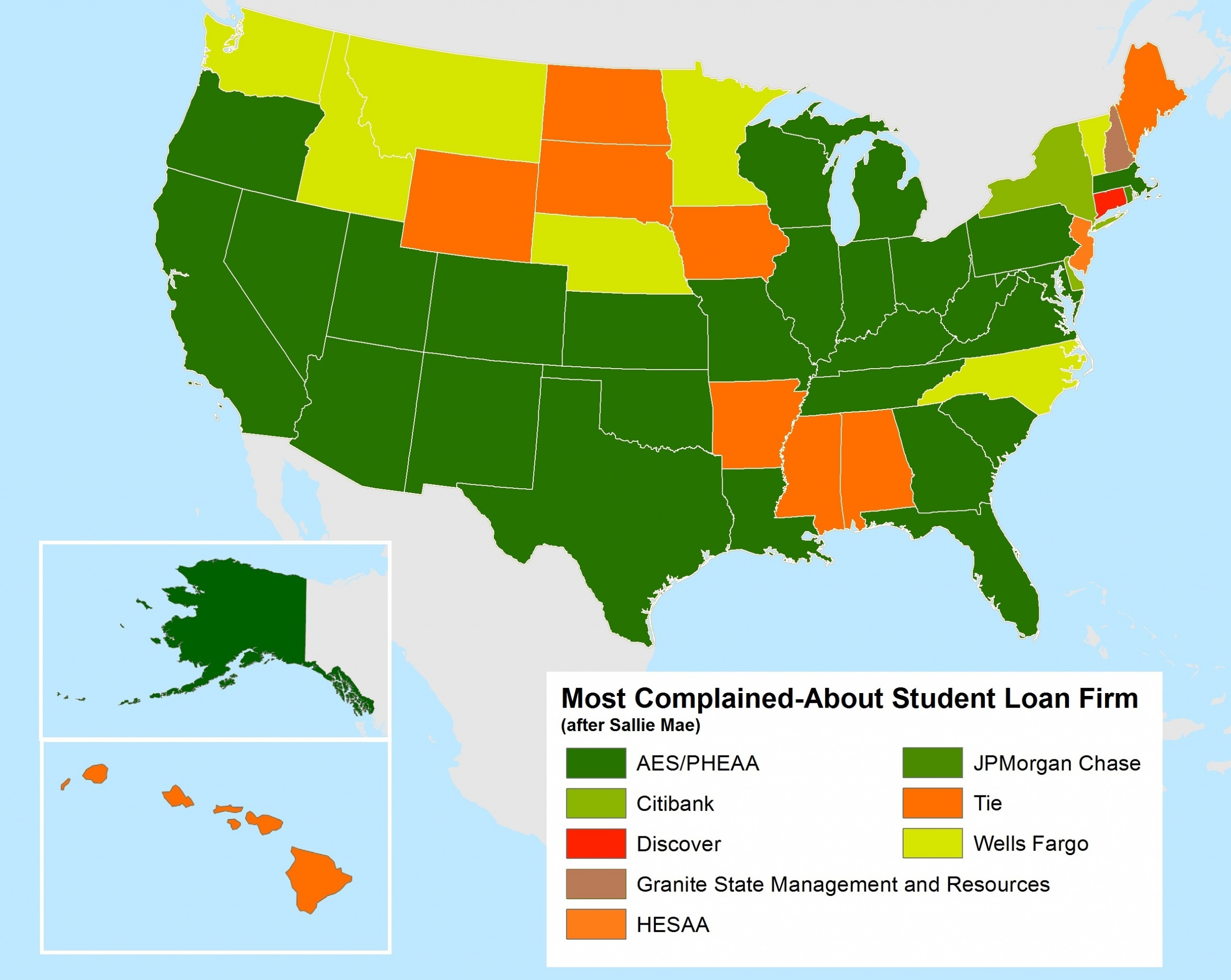

Figure ES-1. Most Complained-About Private Student Loan Firm (other than Sallie Mae) in Each State[i]

Figure ES-2. Complaints about Private Student Loans per 100,000 Student Borrowers, by State

The CFPB is making a significant difference for student borrowers facing difficulty with their financial institutions.

The Consumer Financial Protection Bureau’s Consumer Complaint Database is a key resource for consumer protection. To enhance the effectiveness of the CFPB in addressing consumer complaints:

To improve the effectiveness of the CFPB, the agency should:

* As of August 6, 2013

[i] Sallie Mae was the most complained about lender in every state other than Alaska and Minnesota.

Associate Director and Senior Policy Analyst, Frontier Group

Tony Dutzik is associate director and senior policy analyst with Frontier Group. His research and ideas on climate, energy and transportation policy have helped shape public policy debates across the U.S., and have earned coverage in media outlets from the New York Times to National Public Radio. A former journalist, Tony lives and works in Boston.

Policy Associate

Senior Director, Federal Consumer Program, U.S. PIRG Education Fund

Ed oversees U.S. PIRG’s federal consumer program, helping to lead national efforts to improve consumer credit reporting laws, identity theft protections, product safety regulations and more. Ed is co-founder and continuing leader of the coalition, Americans For Financial Reform, which fought for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, including as its centerpiece the Consumer Financial Protection Bureau. He was awarded the Consumer Federation of America's Esther Peterson Consumer Service Award in 2006, Privacy International's Brandeis Award in 2003, and numerous annual "Top Lobbyist" awards from The Hill and other outlets. Ed lives in Virginia, and on weekends he enjoys biking with friends on the many local bicycle trails.