Gideon Weissman

Former Policy Analyst, Frontier Group

Medical debt collectors often employ aggressive tactics and attempt to collect debt from the wrong customers – putting consumers' credit records at risk. Medical debt accounts for more than half of all collection items that appear on consumer credit reports. A review of 17,701 medical debt collection complaints submitted to the Consumer Financial Protection Bureau (CFPB) shows that problems with medical debt collection are widespread and harm Americans across the country.

Millions of Americans are contacted by debt collectors every year over debt related to medical expenses.

Medical debt collectors often employ aggressive tactics and attempt to collect debt from the wrong customers – putting consumers’ credit records at risk. Medical debt accounts for more than half of all collection items that appear on consumer credit reports. A review of 17,701 medical debt collection complaints submitted to the Consumer Financial Protection Bureau (CFPB) shows that problems with medical debt collection are widespread and harm Americans across the country.

Complaints submitted to the CFPB suggest that many consumers contacted about medical debt should not have been contacted in the first place, and that many contacts involve aggressive or inappropriate tactics.

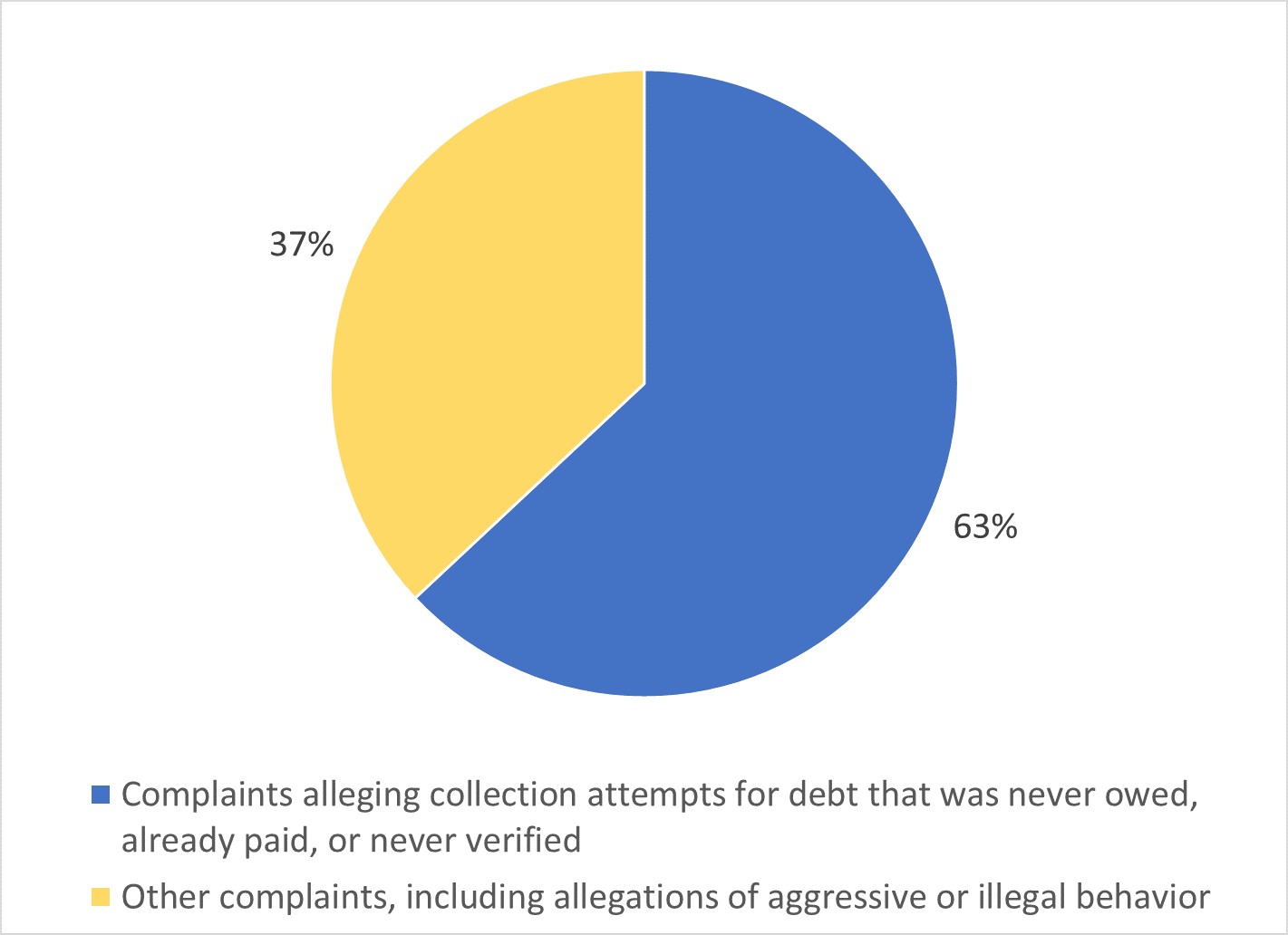

Figure ES-1. Most Complaints Concern Attempts to Collect Debt of Questionable Legitimacy (Debt Consumers Believe Was Already Paid, Never Owed, or Not Verified)

A small number of companies are the subject of a disproportionate amount of total complaints.

Nevada has the most medical debt collection complaints per capita, with 11.4 complaints per 100,000 residents. Florida (9.3), Delaware (9.0), Georgia (7.7) and New Jersey (7.4) have the next highest rates of complaints per capita.

Medical debt collection affects a broad swath of the population and subjects millions of consumers to undue stress and financial harm. State and federal policymakers should work to protect consumers from unfair treatment by medical debt collectors. They should stop attempts to collect debts without proper information and documentation about the debt, stop debt collectors from bringing robo-signed cases in court, crack down on widespread use of threats, harassment and embarrassment in debt collection, and protect consumers from having their credit records unfairly affected by medical debt, among other actions.

Federal policymakers should also defend the CFPB against attempts to eliminate or cripple it, and should continue to ensure the CFPB has the resources, independence and tools at its disposal to effectively protect consumers from all kinds of predatory financial behavior.

Former Policy Analyst, Frontier Group

Director, Consumer Campaign, U.S. PIRG Education Fund

Mike directs U.S. PIRG’s national campaign to protect consumers on Wall Street and in the financial marketplace by defending the Consumer Financial Protection Bureau, and works for stronger privacy protections and corporate accountability in the wake of the Equifax data breach. Mike lives in Washington, D.C.