Corporate Tax Reform Should Discourage Offshore Tax Dodging

At the end of July, President Obama reignited the debate on corporate tax reform, proposing to reduce corporate tax rates while closing loopholes and exemptions that some companies take advantage of. Many corporations currently take advantage of the system by artificially shifting earnings on paper to offshore tax havens—countries with very low or nonexistent taxes—to avoid paying taxes in the United States. In a factsheet we worked on with our colleagues at U.S. PIRG, posted here, we argue that tax reform should close offshore tax loopholes rather than open them further.

by Travis Madsen

At the end of July, President Obama reignited the debate on corporate tax reform, proposing to reduce corporate tax rates while closing loopholes and exemptions that some companies take advantage of. On the one hand, the president called for lowering the standard corporate tax rate from 35 percent to 28 percent – with a preferential 25 percent rate for manufacturers. On the other hand, the president proposed to close exemptions and loopholes to increase revenue, funding investment in jobs and infrastructure.

Offshore tax loopholes are one of the major ways that corporations take advantage of the system. Federal policy allows corporations to postpone indefinitely paying U.S. taxes on profits earned overseas, as long as corporations keep those profits abroad. Many corporations take advantage of the system by artificially shifting earnings on paper to offshore tax havens – countries with very low or nonexistent taxes – to avoid paying taxes in the United States. In 2008, American companies reported 43 percent of their profits from just five tax haven countries – Bermuda, Ireland, Luxembourg, the Netherlands, and Switzerland.

According to our colleagues at U.S. PIRG Education Fund, 82 percent of the top 100 publicly traded companies maintain subsidiaries in offshore tax havens. Altogether, these companies report holding nearly $1.2 trillion offshore, with 15 companies accounting for two-thirds of the offshore cash.

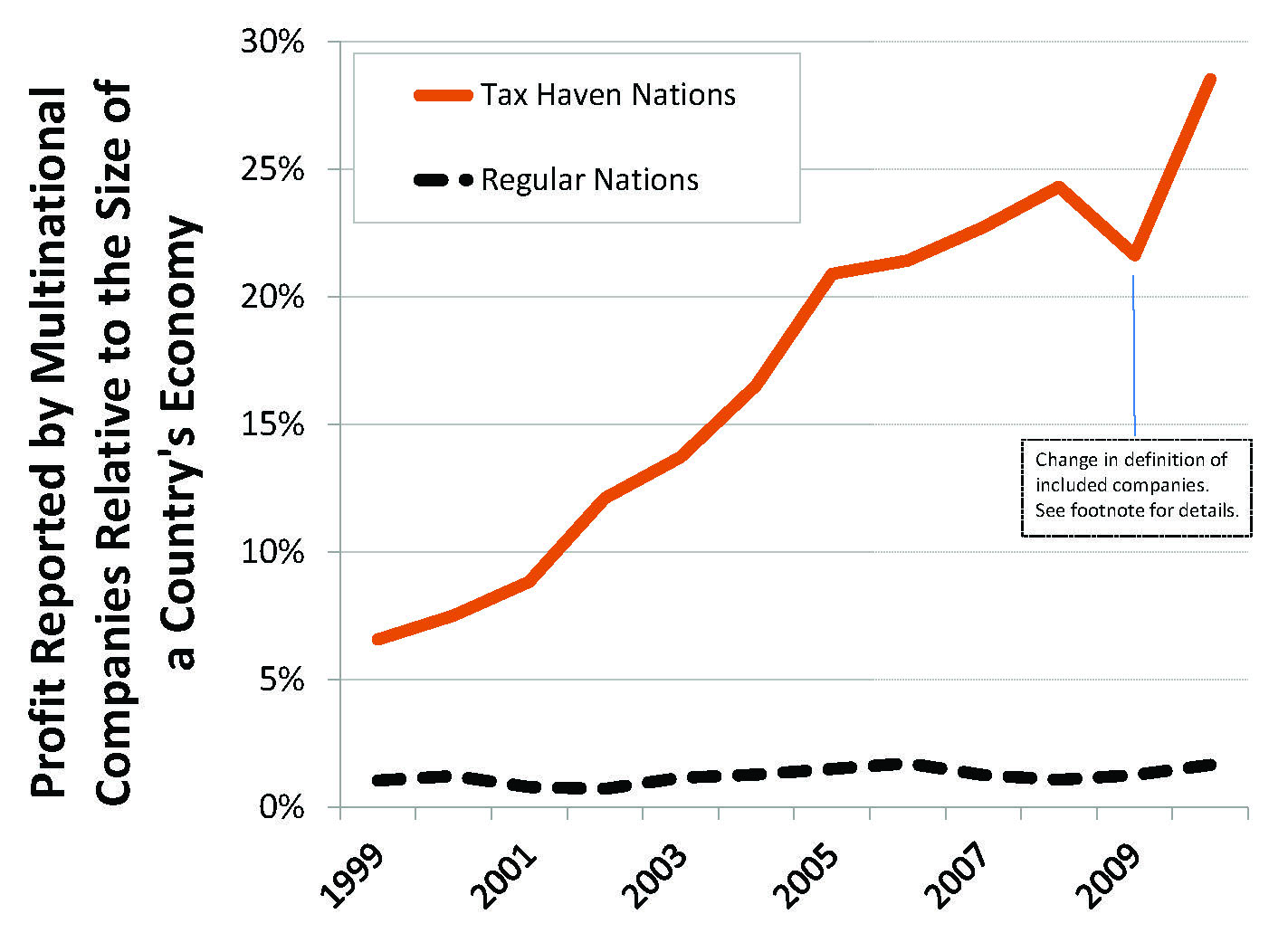

I recently worked with Dan Smith, the tax and budget advocate at U.S. PIRG Education Fund, on a factsheet about offshore tax havens, which you can download here. We documented that profit-shifting activity has increased over the past decade. For example, the amount of profits reported by American companies in Bermuda grew from 260 percent of Bermuda’s overall economy in 1999 to 1,100 percent in 2010—more than a four-fold increase. (See figure.)

Multinational corporations that enjoy the tax benefit of offshore loopholes have been arguing that the United States should shift to what is known as a “territorial” corporate tax system. However, such a system would encourage companies to shift more profits offshore. It would function like a permanent “Get Out of Taxes Free” card from a Monopoly-like game, enabling companies to return income from offshore subsidiaries to the United States without paying taxes.

A “territorial” tax system would function much like a permanent tax repatriation holiday, like the one that Congress enacted in 2004. That move enabled U.S. corporations to return money stored abroad for a highly discounted tax rate. Companies used the extra cash to enrich shareholders or pay down corporate debt rather than to create jobs.

News articles suggest that President Obama may be considering a “one time fee on earnings held overseas,” or another repatriation holiday. Alternatively, he may be considering a “minimum tax on foreign earnings.”

President Obama and his team should seek out opportunities to reduce the ability of the richest corporations to avoid their responsibilities to contribute toward a healthy society for all of us and end the practice of deferring taxes on corporate income generated (or ingeniously shifted) abroad.