Meryl Compton

Policy Associate

College students across the U.S. are at risk of being taken advantage of by banks that pay colleges to market checking accounts directly to students. These campus debit card accounts can come with high and unexpected fees that put college students, many of whom are managing their own finances for the first time, at risk.

College students across the U.S. are at risk of being taken advantage of by banks that pay colleges to market checking accounts directly to students. These campus debit card accounts can come with high and unexpected fees that put college students, many of whom are managing their own finances for the first time, at risk.

Campus debit cards are often used to disburse financial aid refunds when students have funds left over after paying tuition and fees. While students always have the option to receive these refunds in their own pre-existing checking accounts, some banks partner with schools to offer students new checking accounts to receive these funds. Under some agreements, banks are permitted to market their campus debit cards aggressively to the entire student body.

Campus debit cards offered by banks and financial firms can either be in the form of student IDs with built-in banking functions or separate, freestanding cards. There are at least 1.1 million students using campus debit cards, and while these cards can be useful tools for students receiving financial aid or refunds, those that are marketed on campus can come at a cost, particularly to those students who are more vulnerable to high fees, such as first-generation students and those from low- and moderate-income backgrounds.

Most students are protected under recent rules established by the Department of Education (ED), but a few banks continue to put students in harm’s way and require more stringent oversight.

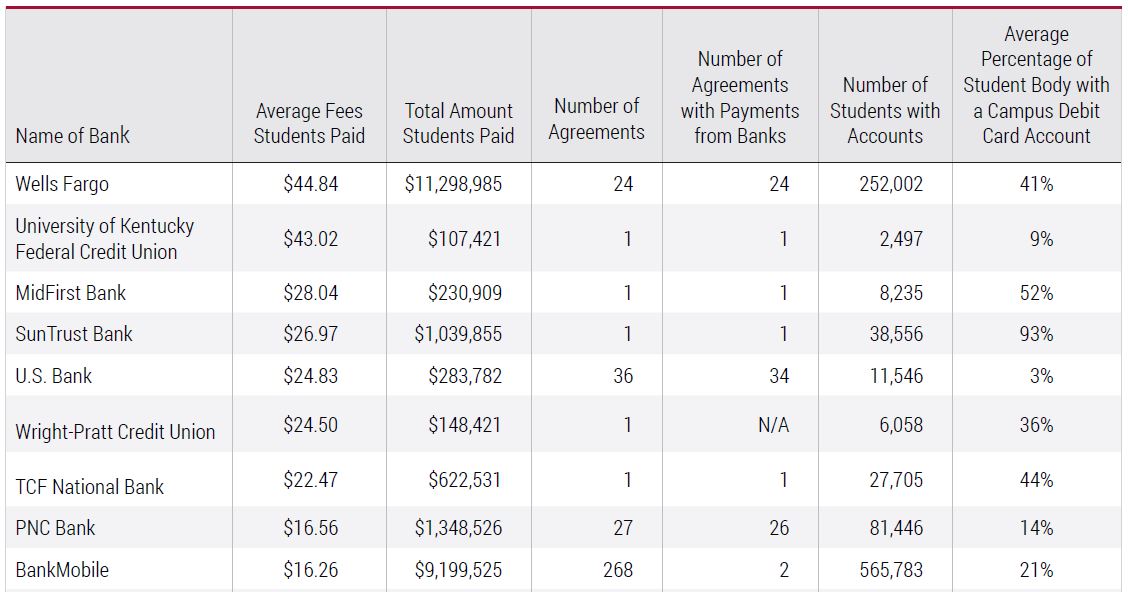

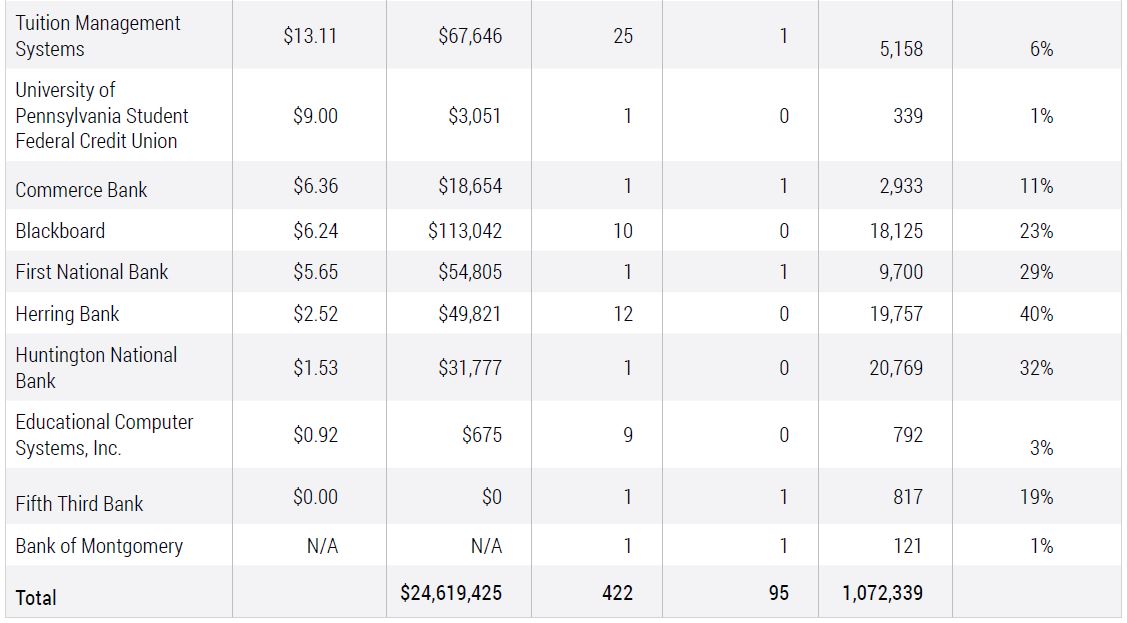

Despite the hundreds of colleges sponsoring low and fee-free student accounts, campus debit card agreements still cost students across the country millions each year. Students nationwide paid more than $24.6 million in fees related to their campus debit card accounts in the most recently available contract year for which their schools reported data to the ED.

Banks that pay colleges for the opportunity to market directly to their students often have higher fees associated with their campus debit card accounts.[i] Based on colleges’ self-reported data that were identified in this analysis:

Table ES-1: Costs and Payments of Banks and Financial Institutions Offering Campus Debit Cards in the Most Recently Available Contract Year[iii]

Notes: 1) The average and total fees students paid are based only on agreements with reported fee data. 2) The total number of student accounts includes all accounts, regardless of whether or not the school reported fee data. 3) Both U.S. Bank and Wright-Pratt Credit Union have one school that did not report data for the flow of money between the school and its partner bank. 4) For four U.S. Bank agreements and two Educational Computer Systems, Inc. agreements, the schools reported the number of accounts to be “Less than 30.” For these cases, this analysis assumes there were 29 accounts. 5) The average percent of the student body with BankMobile accounts does not include five agreements where accurate enrollment data could not be obtained. 6) First National Bank has one agreement, under which it both pays and receives payment from Colorado State University.

Wells Fargo is one of the leading banks offering paid marketing deals that tend to have higher fees for students. Of the 95 schools with reported paid marketing agreements, 24 partnered with Wells Fargo.

Fees and “push marketing” associated with campus debit cards offered through paid marketing agreements can threaten students’ financial well-being.

Some campus debit card providers offering paid marketing agreements reached a majority of the student body. Based on analysis of all identifiable agreements, on average, 41 percent of the students at schools partnering with Wells Fargo had a campus debit card account, compared to 14 percent at schools partnering with PNC Bank. This could indicate a more aggressive marketing effort by the school and its partner bank that is intended to reach the wider student population, beyond just students receiving financial aid refunds.

Several banks that offer paid marketing agreements, including Wells Fargo, PNC Bank and U.S. Bank, incentivize schools to maximize the number of campus debit card accounts by providing the schools with a royalty payment based on the number of students or percentage of the student body with an account. Such provisions encourage more aggressive marketing tactics and often lead to a higher percentage of the student body using campus debit cards that could result in high fees.

In the past, the Consumer Financial Protection Bureau (CFPB) was an effective independent watchdog that helped shield consumers from predatory banking practices, but under the leadership of Mick Mulvaney and Kathy Kraniger, its willingness to protect young consumers is in question. Further, under the direction of Secretary Betsy DeVos, the Department of Education, which is ultimately responsible for enforcing regulations on these campus banking relationships, has ignored CFPB analysis showing that there are problems in the campus banking marketplace, and has failed to provide diligent and consistent oversight to schools reporting the details of their cash management contracts.[v]

In order to protect students, existing regulations need to be enforced and stronger, more comprehensive regulations need to be put in place. Banks and financial firms should be prevented from charging exorbitant fees and offering revenue sharing agreements that facilitate “push marketing” on college campuses. Furthermore, because of the clear and persistent problems and high average fees associated with Wells Fargo’s agreements, the Department of Education should consider launching an investigation into Wells Fargo to determine if its accounts are truly in students’ best interests.

[i] For this report, “school” or “college” also covers the districts or networks of schools that also partner with financial institutions. The vast majority of these partnerships are between an individual school and a financial firm, but some regional networks of for-profit schools may have up to twenty participating campuses.

[ii] The 331 schools are those that had reported data for average annual student fees and had at least 250 campus accounts. The benchmark of 250 students with an account was set to focus on schools were debit cards are more widely used, and to exclude schools with a very small number of accounts.

[iii] These numbers include only those schools that reported annual fee data to ED.

[iv] Revenue-sharing provisions were identified through the schools’ published contracts available on their websites.

[v] Letter from Cheryl Parker Rose, Office of Intergovernmental Affairs to Wayne Johnson, U.S. Department of Education, 5 February 2018, archived at http://web.archive.org/web/20190105164555/https://s3.amazonaws.com/files.consumerfinance.gov/f/documents/bcfp_foia_letter-to-department-education_record_2018-02.pdf.

Policy Associate