The federal Affordable Care Act (ACA) included measures to create a stable insurance market where individual consumers could obtain affordable, comprehensive insurance. However, actions by the federal government have lessened weakened the market for individual insurance, limiting consumers’ ability to obtain comprehensive insurance at a reasonable price. A Better Health Insurance Market for Oregon explores how the state can stabilize the market by reducing uncertainty and risk for insurers and encouraging healthier consumers to continue to buy insurance coverage. To achieve long-term stability for all consumers, however, Oregon must also pursue options for reducing the high cost of health care.

The rising cost of health care is driving up the cost of insurance for all consumers, especially for those who buy insurance through the individual market. The federal Affordable Care Act (ACA) included measures to create a stable insurance market where individual consumers could obtain affordable, comprehensive insurance. However, as the federal government has lessened its support of the health care law, the market for individual insurance has weakened, limiting consumers’ ability to obtain comprehensive insurance at a reasonable price.

Oregon can adopt a number of policies to help stabilize the individual insurance market, which is important for those who currently buy insurance there and those who might need to do so in the future. Oregon can stabilize the market by reducing uncertainty and risk for insurers and encouraging healthier consumers to continue to buy insurance coverage. To achieve long-term stability for all consumers, however, Oregon must also pursue options for reducing the high cost of health care.

Health care is expensive, with prices rising annually. This means that insurance is also growing more expensive.

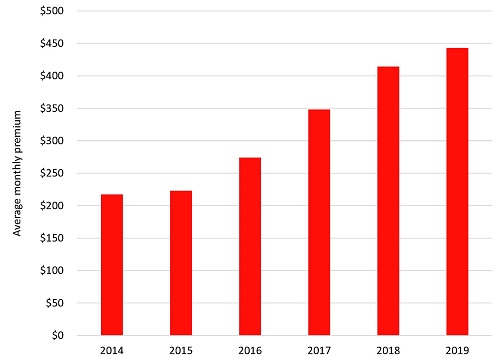

Figure ES-1. The Monthly Cost of the Second-Cheapest Silver-Level Individual Plan in Oregon nearly Doubled from 2014 to 2019[iv]

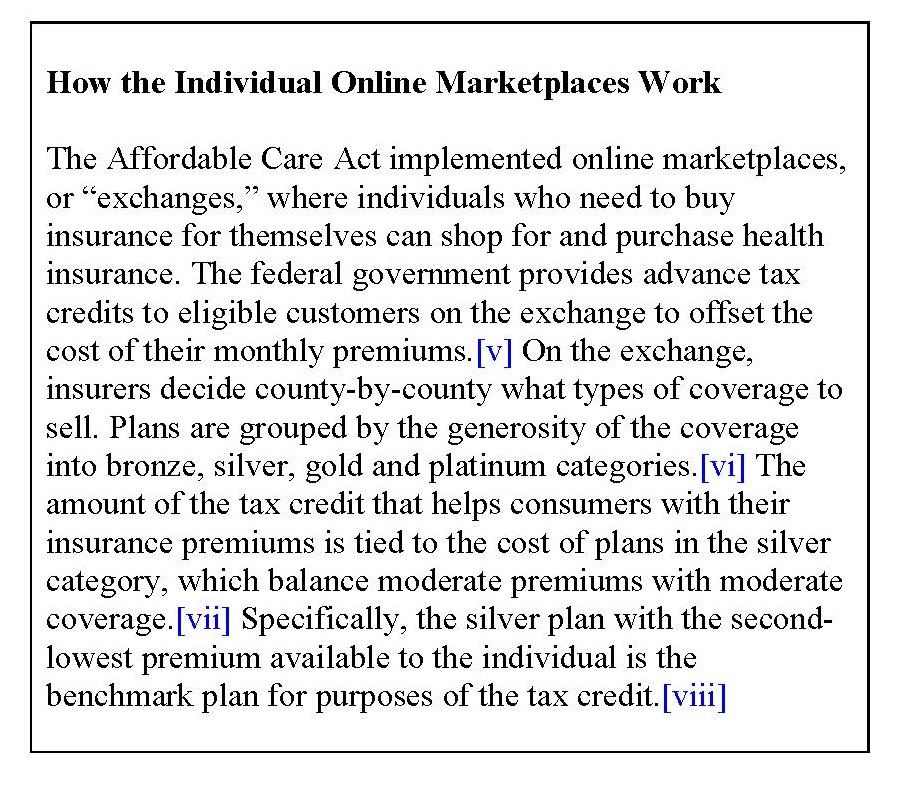

The ACA sought to address multiple problems with health care, including by creating a marketplace where individuals could purchase comprehensive insurance at a reasonable price. (See “How the Individual Online Marketplaces Work.”) Recent federal policy changes, some planned in the ACA and some unexpected decisions by Congress and the Trump administration, coupled with continually rising health care costs, have begun to undermine the individual insurance market. That means it will be more difficult for individual consumers to obtain affordable, comprehensive health insurance coverage.

These forces have begun to destabilize the market for individual health insurance by adding uncertainty and risk for insurers who sell health insurance plans to individuals, driving up insurance premiums and potentially reducing the pool of healthy people purchasing insurance. As healthy people leave the insurance market, only sicker patients remain. This means insurers have higher average health care costs per customer, which leads to higher premiums and further discourages healthy people from purchasing insurance. This market dynamic is sometimes referred to as an “insurance death spiral.”

There are a number of policies Oregon could consider to help limit premium increases, maintain enrollment by healthier individuals and stabilize the individual insurance market so that it remains a valid route for Oregonians to obtain health coverage.

Many of the steps that Oregon could take to stabilize the individual insurance market will be hard to maintain in the face of ever-increasing health care costs. To truly stabilize the individual health insurance market, maintain employer-based coverage, and keep government health care spending to a reasonable level, Oregon must broaden its efforts to address the underlying problem of high and rising health care costs. The state should seek opportunities to reduce health care spending by all payers in the state, while at the same time maintaining or improving the quality of care.

photo: Valeriya/istockphoto

[i] Centers for Medicare & Medicaid Services, National Health Expenditure Data: Health Expenditures by State of Residence, June 2017, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsStateHealthAccountsResidence.html.

[ii] Centers for Medicare and Medicaid Services, National Health Expenditure Data: Historical, 8 January 2018, available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical.html.

[iii] Kaiser Family Foundation, Marketplace Average Benchmark Premiums, 2014-2019, accessed 16 January 2019, at https://www.kff.org/health-reform/state-indicator/marketplace-average-benchmark-premiums/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D.

[iv] Ibid. KFF looked up the cost for a 40-year-old in each county and weighted the results by county plan selections. 2019 data reflect approved rates.

[v] Internal Revenue Service, Questions and Answers on the Premium Tax Credit, 16 March 2018, archived at https://web.archive.org/web/20181230090102/https://www.irs.gov/affordable-care-act/individuals-and-families/questions-and-answers-on-the-premium-tax-credit.

[vi] Centers for Medicare and Medicaid Services, The “Metal” Categories: Bronze, Silver, Gold & Platinum, accessed 17 October 2018, archived at https://web.archive.org/web/20181017174557/https://www.healthcare.gov/choose-a-plan/plans-categories/.

[vii] Louise Norris, “What Is a Benchmark Plan Under the ACA?” VeryWell Health, 9 April 2018, archived at https://web.archive.org/web/20190320000848/https://www.verywellhealth.com/under-the-aca-what-is-a-benchmark-plan-4160065.

[viii] Ibid and see note 6.

[ix] In December 2017, Congress passed the Tax Cuts and Jobs Act and eliminated the individual mandate penalty, effective January 1, 2019.

[x] Regence BlueCross BlueShield of Oregon, Filing for H16I Individual Health – Major Medical/H16I.005A Individual – Preferred Provider (PPO), SERFF Tracking #: RGOR-131494722, accessed 13 March 2019 at https://www4.cbs.state.or.us/exs/ins/rates2/index.cfm?B64=nZzVWZjFGdvljbo12bl1nLoN3bfdGZj9WbtdCd0Z1az9mcfZmZslWan52XvRzYx0%0A%0DDMxAQO%3D%3D, and Health Net Health Plan of Oregon, Inc., Filing for H16I Individual Health – Major Medical/H16I.005C Individual – Other, SERFF Tracking #: HNOR-131466265, accessed 13 March 2018 at https://www4.cbs.state.or.us/exs/ins/rates2/index.cfm?B64=nZzVWZjFGdvljbo12bl1nLoN3bfdGZj9WbtdCd0Z1az9mcfZmZslWan52XvRzYx0%0A%0DDMwAQO%3D%3D.

[xi] Jeff Manning, “Oregon’s Second Health Insurance Co-op to Be Liquidated,” The Oregonian/OregonLive, 8 July 2016, archived at https://web.archive.org/web/20190320001047/https://www.oregonlive.com/business/2016/07/oregons_second_health_insuranc.html.

[xii] Slightly under half of individuals who obtain insurance through the individual market do not receive a tax credit to help reduce their monthly premiums. Seventy-four percent of participants in the exchange qualified for a tax credit in 2018, per Department of Consumer and Business Services, Oregon Health Insurance Marketplace: 2017 Annual Report, 15 April 2018, archived at https://web.archive.org/web/20190320001143/https://www.oregonlegislature.gov/salinas/HealthCareDocuments/3.%20Marketplace-Annual-Report%202017%20-%20Released%204.15.18.pdf. In 2017, 3.7 percent of Oregonians obtained insurance through the exchange and 1.5 percent bought individual plans off the exchange, per Oregon Health Authority, 2017 Oregon Health Insurance Survey: Early Release Results, 5 December 2017, archived at https://web.archive.org/web/20190320001244/https://www.oregon.gov/oha/HPA/ANALYTICS/InsuranceData/2017-OHIS-Early-Release-Results.pdf.

[xiii] Louise Norris, “The Problem with Association Health Plans,” Healthinsurance.org, 1 June 2018, archived at https://web.archive.org/web/20180919122003/https://www.healthinsurance.org/blog/2018/06/01/the-problem-with-association-health-plans/.

[xiv] Linda Blumberg, Matthew Buettgens and Robin Wang, Urban Institute, Updated: The Potential Impact of Short-Term Limited-Duration Policies on Insurance Coverage, Premiums and Federal Spending, March 2018, archived at https://web.archive.org/web/20181129161531/https://www.urban.org/sites/default/files/publication/96781/2001727_updated_finalized.pdf, and Jeff Manning, “For Oregonians, Rate Hikes Ease But Still Sting: 2019 Insurance Guide,” The Oregonian/OregonLive, 28 October 2018, archived at https://web.archive.org/web/20190320041726/https://www.oregonlive.com/business/2018/10/in_oregon_rate_hikes_ease_but.html.

[xv] Markian Hawryluk, “Oregon Could Relaunch State Insurance Exchange,” The Bulletin, 13 May 2018, archived at https://web.archive.org/web/20180710035141/https://www.bendbulletin.com/localstate/6232435-151/oregon-could-relaunch-state-insurance-exchange.

[xvi] Ibid.

Associate Director and Senior Policy Analyst, Frontier Group

Elizabeth Ridlington is associate director and senior policy analyst with Frontier Group. She focuses primarily on global warming, toxics, health care and clean vehicles, and has written dozens of reports on these and other subjects. Elizabeth graduated with honors from Harvard with a degree in government. She joined Frontier Group in 2002. She lives in Northern California with her son.

Policy Associate