Gideon Weissman

Former Policy Analyst, Frontier Group

The tactics used by the debt collection are a growing source of consumer pain; they include incessant calling, threats of arrest, and damaged credit reports – while often targeting the wrong consumer, and often violating the law. To gain insight into the impact on consumers of medical debt collection, we turned to the consumer complaint database of the Consumer Financial Protection Bureau (CFPB) for our new report, Medical Debt Malpractice: Consumer Complaints About Medical Debt Collectors, and How the CFPB Can Help.

In recent years, America’s complicated and expensive health care system has spawned an enormous medical debt collection industry. These aren’t just companies that assist hospitals in collecting past-due bills; rather, the industry is a sprawling web of debt buyers, who purchase debt at cents on the dollar from health care providers and from each other, often with little information beyond names and amounts, and then work with collection agencies and debt collection law firms to extract payment however they can.

The tactics used by the debt collection are a growing source of consumer pain; they include incessant calling, threats of arrest, and damaged credit reports – while often targeting the wrong consumer, and often violating the law. To gain insight into the impact on consumers of medical debt collection, we turned to the consumer complaint database of the Consumer Financial Protection Bureau (CFPB) for our new report, Medical Debt Malpractice: Consumer Complaints About Medical Debt Collectors, and How the CFPB Can Help.

The Consumer Complaint Database, which began accepting consumer complaints in 2011, has turned into an important tool for understanding consumer interactions with financial companies. We’ve used the database as the basis for a number of reports now, covering topics like the broader debt collection industry, credit cards and overdraft fees.

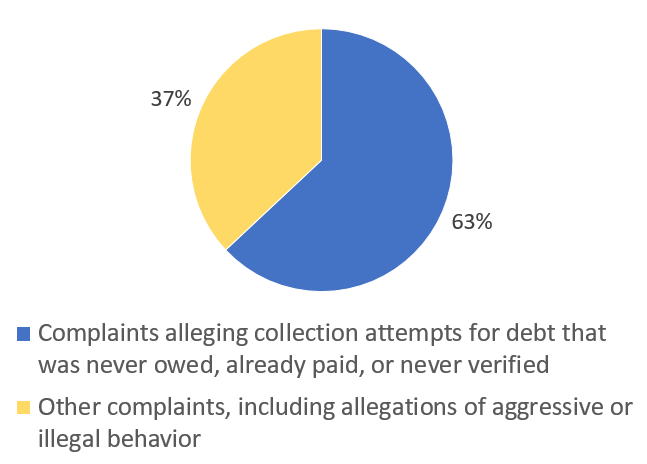

Consumers’ most common complaints about medical debt collection are – incredibly – about attempts to collect debt that consumers do not believe they owe. More than 60 percent of complaints assert that the consumer’s debt was already paid, was never owed, or was not verified by the collector prior to collection. We also found thousands of complaints concerning aggressive and illegal tactics used by collectors, including threats of arrest and embarrassment, and incessant calling. And we found that more than a third of complaint narratives (consumer-written stories included with complaints) include the term “credit report,” worth noting given the often unfair and inaccurate impact of medical debt on consumer credit.

This report shows the importance of a strong CFPB – not only is it the most important federal agency for protecting consumers in the financial marketplace (which includes the debt collection industry), it is also the entity that collects and aggregates complaint data that provide an invaluable consumer’s-eye view of the financial services industry. Since it began operations in 2010, the CFPB has provided nearly $12 billion in relief to more than 29 million consumers.[pdf] Ongoing calls to weaken the CFPB threaten to harm consumers and take away one of their most valuable resources. Today, with the consumer marketplace growing in complexity and creating new tricks and traps for consumers all the time, the CFPB is more important than ever.

Former Policy Analyst, Frontier Group